Wallison's proposal for cross border financial resolutions

The Lehman bankruptcy, the seminal event of the credit crisis, ‘shows how a territorial system can destroy value and create arbitrary and unnecessary risks and losses for creditors’ according to leading member of the US Congress' Financial Crisis Inquiry Commission, Peter J Wallison, formerly legal counsel to US president Ronald Reagan. The editor, Ken O’Brien, spoke to him about the details of a scheme he has developed to resolve the problem, to the potential benefit of jurisdictions worried about financial risks arising from cross-border resolutions.

June 2010: The risk to small countries who host financial centres, such as Ireland, Luxembourg, and many of the British offshore centres and Crown dependencies such as the Channel islands is currently in vogue, as it is with regulators in larger centres, as evidenced by a report just published by the Institute for International Finance, which puts the issue at the very top of their agenda.

With regulation officially at the top of the agenda at the Toronto G20 summit, the issue also should bear attention there.

Peter J Wallison believes he has a fix, and in an interview with Ken O'Brien, he sets out his solution, an idea that, had it existed when Lehmans failed, would have saved a lot of bother, and would eliminate a major part of the transnational risk that regulators now worry about, and which threaten the globalisation of finance, and even raise the spectre of a return to the financial autarky (that Keynes, among others, contemplated in the 1930s).

The problem is that bankruptcy systems are territorial and national, given the traditional jurisdiction of bankruptcy courts. When banks are in difficulties, it becomes reminiscent of the desparate observation of the Icelandic Prime Minister memorably on the night of Iceland’s demise, ‘it’s every man for himself’.

To counter this, Wallison proposes what he calls a ‘debtor selection system’. It has the merit of simplicity, and workability. Once established , by an internaitonal protocol, he believes, financial centres around the world would feel compelled to comply, and a domino effect across international boundaries and regions of all kinds could see the system established.

One of the biggest problems is what to do about the bankruptcy of large institutions that are globally active, he says. ‘Another of the lessons of the Lehman bankruptcy is that the insolvency laws don’t work very well when we are dealing with a firm that has substantial assets in many different countries. In general, the world’s bankruptcy systems are territorial, which means that the courts or equivalent institutions in each country have control over the assets of a bankrupt firm that remain within their borders at the time it or its creditors petition for bankruptcy elsewhere. These assets are then routinely used to compensate local claimants. The US is no exception. Bankruptcy courts in the US are reluctant to release funds to foreign jurisdictions if that will reduce the returns to US claimants.’

The Lehman case, says Wallison, was, in this sense, a classic. ‘It happens that each night Lehman routinely repatriated to New York all the cash in its global system, and when it filed for bankruptcy at 4am on Monday, September 15, 2008, it still had custody of much of the cash that its various foreign subsidiaries used for daily operations. When the Lehman petition was filed the New York bankruptcy court took control of the action and the cash.’ ‘The Lehman case shows how a territorial system can destroy value and create arbitrary and unnecessary risks and losses for creditors’, he says.

‘With a lot of the Lehman cash still in New York, and under the control of the US court, Lehman subsidiaries abroad were forced to declare bankruptcy. If these firms had had access to their cash resources, they might have survived the parent’s bankruptcy and added substantially to the value of the Lehman enterprise as a whole. Their wholesale bankruptcy reduced the values available to US and foreign creditors alike, although most of the losses probably fell on the foreign creditors of Lehman’s subsidiaries outside the United States. The US creditors of the company were probably the beneficiaries of this arbitrary outcome, although they also lost the going concern value of the whole Lehman enterprise.

‘As many scholars have pointed out, the solution to this problem is a system for the central administration of a bankrupt estate with operations around the world. There are strong policy arguments for this, since the uncertainties associated with recoveries from a bankrupt company can raise risk premia and the costs of financing. As the financial world becomes increasingly global, dealing with this problem will become increasingly difficult yet increasingly important.

‘Although a favorite of scholars, a universal system - in which all developed countries agree on a single insolvency system - seems out of reach’, he says. ‘There are simply too many values, and issues at stake in each country. As lawyer Alexander Kipnis has observed, it has been difficult to come to agreement on a universal insolvency system even in the EU. These countries, he notes, ‘exhibit a dizzying array of different choices about the scope of the estate, claim recognition, class treatment, creditor priority, available remedies, and just about all other aspects of bankruptcy proceedings. It is this rich diversity of policy choices on the global scale that makes transnational bankruptcy so unpredictable and a uniform regime desirable. . . If substantive consensus cannot be achieved in Europe, there is little hope that a consensus on substantive law can be had on a global scale.’

What, then, is the solution? One possibility is what he calls the ‘Debtor Selection System’.

He explains: ‘Under this system, each financial institution would select the national insolvency system under which it will be resolved in the event of its bankruptcy. Creditors, by lending to these firms, would in effect agree to the choice. By international treaty, signatory countries would agree to enforce the rulings of the court or other body that resolves insolvencies in the country chosen by the financial firm. This does not require any country to change its insolvency laws, but it does create incentives for countries to adopt insolvency rules that are attractive to both debtors and creditors, and court systems that operate expeditiously and free of political influence.

If such a system had been in place at the time of Lehman’s bankruptcy, the outcome would have been considerably better. ‘If we assume that Lehman had chosen the US bankruptcy system, and that most of the cash was in New York at the time the petition was filed, the US court would have known that it had control over the worldwide operations and assets of Lehman, even if it released the cash to the subsidiaries. Lehman’s creditors everywhere - whether creditors of the parent or the subsidiaries - would have been treated equally and consistently according to the bargains they had initially struck, knowing what resolution regime would be applied and how it would operate for their particular class’.

‘We are a long way now from such a system, but as the financial market becomes increasingly global in the years ahead we are going to have to find a way to make the allocation of losses in bankruptcy less arbitrary than what occurs in the territorial system that prevails today.

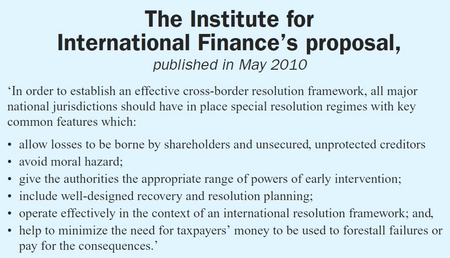

The Institute for International Finance, in a major report, published at the end of May www.iif.com/press/press+148.php surveys the field and calls for progress towards a resolution of the problem.

Editor: ‘Do you agree with the general thrust of the IIF’s proposals (for example, cutting out moral hazard) and would it mesh in well with your plan ? (They seem to think something more complex than what you suggest is needed, - and seem to feel innovative approaches are needed)?

Wallison: Yes, I think it’s quite consistent with my plan. The IIF is calling for an ‘international framework on cross-border resolution’ and that’s exactly what debtor selection plan is designed to provide.

Q: ‘It seems to me that your proposal ticks all the boxes they call for, do they?

A: ‘Yes, they call for convergence of national resolution regimes, a lead resolution authority and consideration of a means to address fairness in the allocation of assets between jurisdictions and entities. These are all objectives of the debtor selection system.

Q: ‘Furthermore, would you say that your’s has the advantage of innovativeness, and simplicity?

A: Yes, one of the most favorable aspects of the debtor selection system is its simplicity; it does not require governments to agree on the same resolution principles, but only that they agree to enforce the resolution regime of the jurisdiction that the debtor selected at some point in the past.

Q: What kind of international treaty would you envisage. How many countries, promoted by what body, how enforced, and in what possible time frame. Might it even be a runner at the G20 meeting?

A: I would envision a treaty or protocol in which the major countries with developed or mature economies agree to enforce within their own borders the resolution regime of any other signatory country if that resolution regime was selected in advance by an internationally active firm. It isn’t necessary that all countries sign the treaty of protocol. Even if only a few countries agreed to adhere to the treaty’s provisions, that would create substantial pressure for others to sign so their citizens could obtain the benefits of the system.

|

| Wallison: 'We are going to have to find a way to make the allocation of losses in bankruptcy less arbitrary than in the territorial system that prevails today'. |

With regulation officially at the top of the agenda at the Toronto G20 summit, the issue also should bear attention there.

Peter J Wallison believes he has a fix, and in an interview with Ken O'Brien, he sets out his solution, an idea that, had it existed when Lehmans failed, would have saved a lot of bother, and would eliminate a major part of the transnational risk that regulators now worry about, and which threaten the globalisation of finance, and even raise the spectre of a return to the financial autarky (that Keynes, among others, contemplated in the 1930s).

The problem is that bankruptcy systems are territorial and national, given the traditional jurisdiction of bankruptcy courts. When banks are in difficulties, it becomes reminiscent of the desparate observation of the Icelandic Prime Minister memorably on the night of Iceland’s demise, ‘it’s every man for himself’.

To counter this, Wallison proposes what he calls a ‘debtor selection system’. It has the merit of simplicity, and workability. Once established , by an internaitonal protocol, he believes, financial centres around the world would feel compelled to comply, and a domino effect across international boundaries and regions of all kinds could see the system established.

One of the biggest problems is what to do about the bankruptcy of large institutions that are globally active, he says. ‘Another of the lessons of the Lehman bankruptcy is that the insolvency laws don’t work very well when we are dealing with a firm that has substantial assets in many different countries. In general, the world’s bankruptcy systems are territorial, which means that the courts or equivalent institutions in each country have control over the assets of a bankrupt firm that remain within their borders at the time it or its creditors petition for bankruptcy elsewhere. These assets are then routinely used to compensate local claimants. The US is no exception. Bankruptcy courts in the US are reluctant to release funds to foreign jurisdictions if that will reduce the returns to US claimants.’

The Lehman case, says Wallison, was, in this sense, a classic. ‘It happens that each night Lehman routinely repatriated to New York all the cash in its global system, and when it filed for bankruptcy at 4am on Monday, September 15, 2008, it still had custody of much of the cash that its various foreign subsidiaries used for daily operations. When the Lehman petition was filed the New York bankruptcy court took control of the action and the cash.’ ‘The Lehman case shows how a territorial system can destroy value and create arbitrary and unnecessary risks and losses for creditors’, he says.

‘With a lot of the Lehman cash still in New York, and under the control of the US court, Lehman subsidiaries abroad were forced to declare bankruptcy. If these firms had had access to their cash resources, they might have survived the parent’s bankruptcy and added substantially to the value of the Lehman enterprise as a whole. Their wholesale bankruptcy reduced the values available to US and foreign creditors alike, although most of the losses probably fell on the foreign creditors of Lehman’s subsidiaries outside the United States. The US creditors of the company were probably the beneficiaries of this arbitrary outcome, although they also lost the going concern value of the whole Lehman enterprise.

‘As many scholars have pointed out, the solution to this problem is a system for the central administration of a bankrupt estate with operations around the world. There are strong policy arguments for this, since the uncertainties associated with recoveries from a bankrupt company can raise risk premia and the costs of financing. As the financial world becomes increasingly global, dealing with this problem will become increasingly difficult yet increasingly important.

‘Although a favorite of scholars, a universal system - in which all developed countries agree on a single insolvency system - seems out of reach’, he says. ‘There are simply too many values, and issues at stake in each country. As lawyer Alexander Kipnis has observed, it has been difficult to come to agreement on a universal insolvency system even in the EU. These countries, he notes, ‘exhibit a dizzying array of different choices about the scope of the estate, claim recognition, class treatment, creditor priority, available remedies, and just about all other aspects of bankruptcy proceedings. It is this rich diversity of policy choices on the global scale that makes transnational bankruptcy so unpredictable and a uniform regime desirable. . . If substantive consensus cannot be achieved in Europe, there is little hope that a consensus on substantive law can be had on a global scale.’

What, then, is the solution? One possibility is what he calls the ‘Debtor Selection System’.

He explains: ‘Under this system, each financial institution would select the national insolvency system under which it will be resolved in the event of its bankruptcy. Creditors, by lending to these firms, would in effect agree to the choice. By international treaty, signatory countries would agree to enforce the rulings of the court or other body that resolves insolvencies in the country chosen by the financial firm. This does not require any country to change its insolvency laws, but it does create incentives for countries to adopt insolvency rules that are attractive to both debtors and creditors, and court systems that operate expeditiously and free of political influence.

If such a system had been in place at the time of Lehman’s bankruptcy, the outcome would have been considerably better. ‘If we assume that Lehman had chosen the US bankruptcy system, and that most of the cash was in New York at the time the petition was filed, the US court would have known that it had control over the worldwide operations and assets of Lehman, even if it released the cash to the subsidiaries. Lehman’s creditors everywhere - whether creditors of the parent or the subsidiaries - would have been treated equally and consistently according to the bargains they had initially struck, knowing what resolution regime would be applied and how it would operate for their particular class’.

‘We are a long way now from such a system, but as the financial market becomes increasingly global in the years ahead we are going to have to find a way to make the allocation of losses in bankruptcy less arbitrary than what occurs in the territorial system that prevails today.

The Institute for International Finance, in a major report, published at the end of May www.iif.com/press/press+148.php surveys the field and calls for progress towards a resolution of the problem.

|

Editor: ‘Do you agree with the general thrust of the IIF’s proposals (for example, cutting out moral hazard) and would it mesh in well with your plan ? (They seem to think something more complex than what you suggest is needed, - and seem to feel innovative approaches are needed)?

Wallison: Yes, I think it’s quite consistent with my plan. The IIF is calling for an ‘international framework on cross-border resolution’ and that’s exactly what debtor selection plan is designed to provide.

Q: ‘It seems to me that your proposal ticks all the boxes they call for, do they?

A: ‘Yes, they call for convergence of national resolution regimes, a lead resolution authority and consideration of a means to address fairness in the allocation of assets between jurisdictions and entities. These are all objectives of the debtor selection system.

Q: ‘Furthermore, would you say that your’s has the advantage of innovativeness, and simplicity?

A: Yes, one of the most favorable aspects of the debtor selection system is its simplicity; it does not require governments to agree on the same resolution principles, but only that they agree to enforce the resolution regime of the jurisdiction that the debtor selected at some point in the past.

Q: What kind of international treaty would you envisage. How many countries, promoted by what body, how enforced, and in what possible time frame. Might it even be a runner at the G20 meeting?

A: I would envision a treaty or protocol in which the major countries with developed or mature economies agree to enforce within their own borders the resolution regime of any other signatory country if that resolution regime was selected in advance by an internationally active firm. It isn’t necessary that all countries sign the treaty of protocol. Even if only a few countries agreed to adhere to the treaty’s provisions, that would create substantial pressure for others to sign so their citizens could obtain the benefits of the system.