The battleground for reform - a profile of the emerging global regulatory architecture

A war is raging globally about the form of financial regulation, with the battle raging most fiercely in the United States and Europe. The resolution of the new financial frameworks on either side of the Atlantic is also setting the stage for how Asia and the rest of the world reacts, as the centre of gravity in world economies shifts. We survey the new structures that are emerging and the hot issues.

October 2010: Never since the 1930s has the world seen such a proliferation of new acronyms for newly formed regulatory institutions, or for old organisations given new names than in the Fall/Autumn of 2010. So for readers we provide an overview of the new bodies, their powers, and the reasons for their formation, or reformulation. In this month's issue, we focus on the new structures in the USA, and the European Union. Future issues will see Asia, and other major countries, including the UK, Australia and Canada included.

It is clear, however, that the new framework is just that – an empty institutional framework, that, as ever depends on the quality of the people who will drive it and staff it, and further, on the degree of sense, and consensus, that will inform the process of reforming financial centres regulation after the credit crisis. The jury remains out as to how that will pan out, because, as our review of the issues, and turf wars and controversies raging right across this international regulatory battlefield shows, the final shape of financial regulation remains to be decided.

These focus at their core on how the key issues arising from the credit crisis are being addressed. To the extent that these are being resolved, closure and progress towards stable reform will be achieved.

The credit crisis, first and foremost, was a failure of monetary policy, a view that is reflected in a paper by the chairman of the Federal Reserve Ben Bernanke in September 2010.

A major reason for this was that money supply was measured in too limited a way (and in a way that excluded the shadow banking system that grew up in the 1990s), largely beyond the attention of Central Banks.

The resolution of the banking crisis will depend on how regulators get to grips with fixing this problem, both at Central Bank level, at international cooperation level, and down to securities regulation and accounting levels. Thus issues such as central party clearing of credit derivatives arrangements are taking centre stage in the new regulatory architecture, and issues such as the Basle Committee rules for bank capital (centrally crucial), and accounting conventions, adopted by FASB and IASB, are also at the core of the story. In all of these areas, battles and controversies still rage, and how key issues are resolved will tell the tale.

At the end of the day, the credit crisis was a problem of unsound money – a problem, largely of the 2000s. Before that, the world had seen the 'death of inflation', and the decade of the 1990s ended with the price of gold at $300, down 25 p.c. on what it was a decade earlier. Now the performance of the price of gold on a daily basis is signalling to us that the problem is far from resolved. In that context, the murky shapes emerging of the new global regulatory architecture may hopefully provide optimism that a stable and solid global framework can be put in place.

Global

The Group of 20 (G20)

The Group of 20 morphed out (in 2008) of the G7 and G8 of the 1970s and 1980s as the bi-annual forum of global heads, at times meeting to coordinate macro-economic strategies to becoming the primary politicians forum for agreeing joint initiatives about the regulatory and banking framework. As a political forum its antecedents stretch back in history, some might argue going back, perhaps, to the Treaty of Vienna, or even before, the Treaty of Westphalia (1648).

Today it drives the tax agenda of the OECD, and bank regulatory matters. Its expansion from the G8 to the G20 was also accompanied by a more specific financial stability mandate. Its next meeting is in Seoul in November. However, as with all global bodies, its powers are suasive, and informal, and derive their force from reputational force, such as the OECD 'name and shame' approach of publishing blacklists of aberrant 'tax havens'.

Head: Lee Myung-bak

Head Office (Current): Seoul, Rep Korea

International Monetary Fund (IMF)

The IMF, like its counterparts, the World Bank, and the OECD, are institutions that were formed at Bretton Woods, at the seminal gathering of victorious governments after WW2, and which approved the 'Marshall Plan' for the aiding of recovery in Europe. These bodies were set up as part of the Marshall Plan architecture.

The IMF today has a newly rejuvenated role, thanks to sovereign debt difficulties, most notably in Europe, and its role in coordinating finance from member states in general, as well as the European Union to aid Greece, represented an internationalisation of the debt crisis beyond the confines of the European Union. It may also gain enhanced influence in the currency policy sphere.

Head: Dominique Strauss-Kahn

Head Office: Washington, DC, USA

The World Bank

The World Bank, with its developmental mandate continues to pursue supplementary support programs, as well as support activities such as the publication of its influential 'Ease of Doing Business' Surveys.

Head: Robert Zoellick

Head Office: Washington, DC, USA

United States of America

US Treasury

In pole position, the US Treasury will orchestrate the workings of the newly established Financial Stability Oversight Council, through its secretariat, The Office of Financial Research (OFR), which will operate from within the Treasury Department.

Head: Timothy Geithner

Head Office: Washington, DC, USA

The Federal Reserve Board

The Dodd Frank Bill has unleashed the so-called “Banking Agencies” with new powers that raises their status to that of the Fed on the Financial Stability Oversight Council. The fears are that these will prove a route for political interference with Fed oversight and enforcement of monetary policy.

Head: Ben Bernanke

Head Office: Washington, DC, USA

Congress & Financial Committees

Congressional representatives, and committees, for example the Financial Crisis Committee, which reports this Fall, exert major influence, which can find their way into interference in policy via the new channels opened up by Dodd-Frank.

Head: Nancy Pelosi

Head Office: Washington, DC, USA

European Union

Economic and Financial Affairs Council (ECOFIN)

Chair: Didier Reynders, Belgian Deputy PM and Minister for Finance

The Council of Finance Ministers of the sovereign members of the European Union. The European Parliament proposes, and votes on EU supranational legislation, drafted by the European Commission, which is the civil service of the EU, directed by EU Commissioners, each appointed for a term co terminus with the life of the European Parliament. Financial services regulation is the responsibility of DG Markt (Internal Market Directorate) (Head: Commissioner Michel Barnier), and credit and banking DG ECFIN (Commissioner Olli Rehn). The EU Parliament Economic & Monetary Affairs Committee appointed from MEPs (Chair: Sharon Bowles MEP) oversees legislation and financial services regulatory affairs.

European Central Bank (ECB)

The ECB, as the federal central bank for the euro, is in the eye of the global financial storm, alongside its US counterpart, the Fed. As architect of the first major truly global currency in history, the experiment of the euro has been tarnished by the credit crisis, and, latterly by the sovereign debt crisis in the EU. The president of the ECB JC Trichet has been reaffirmed as pole player in charge of the new EU Bank regulatory body, the European Systemic Risk Board (ESRB) attached to the ECB.

CEO: Jean Claude Trichet

Head Office: Frankfurt, Germany

Global

Financial Stability Board (FSB)

The FSB, a good idea in theory, but possibly bad in practice, is lauded as the ‘potential fourth pillar of the Bretton Woods system’ is perhaps the most obvious early creation of the credit crisis. It sprung from the idea that because the credit crisis was 'global' what was needed was a global body that dealt with global systemic risk issues. The danger, as with all such bodies, is that it might distract attention from the role of national central banks in running their own money supplies, and regulating their own banking, and shadow banking systems. The most important potential role for the FSB would be the promotion of currency stability (and flexibility) in the world, so that countries and currency zones pursuing sound money strategies (a) could be persuaded of the value of sound money, and strong currencies, and (b) encouraged, or incentivised in some way, to pursue such strategies. As Asia, and Asian centres have been exemplary in the 2000s, compared with their Atlantic counterparts, perhaps the headquarters of the FSB could be moved to Beijing at an appropriate time in the future, with the Chinese dropping as a quid pro quo their suggestion that IMF SDRs replace the US dollar as the de facto global reserve currency?

HEAD: Mario Dhragi

Head Office: Basle, Switzerland

The Basel Committee on Banking Supervision/Bank for International Settlements (BIS)

When the history of the 21st century's credit crisis (history's first credit derivatives crisis) is written, the potential role of the Basle Committee in defining the new global ground rules for bank leverage, may loom large. If it does so wisely, including sensible measures for the measurement of bank capital, and how credit derivatives should be properly accounted for in the future, it will emerge as having a pivotal role.

Head: Nout Wellink

Head Office: Basle, Switzerland

United States of America

- The Financial Stability Oversight Council & OFR

- The Office of Financial Research (OFR)

- The Federal Reserve Board

- Office of the Comptroller of the Currency ( OCC)

- Office of Thrift Supervision (OTS)

- Federal Deposit Insurance Corporation (FDIC)

- The Fed, OCC, OTS, and FDIC (together, the “Banking Agencies”)

European Union

- European Central Bank (ECB)

- European Systemic Risk Board (ESRB) (Attached to the ECB)

- European System of Financial Supervisors (ESFS)

- The European Banking Authority (EBA)

Global

International Accounting Standards Board (IASB)

Indicating that true global leadership in finance remains in the United States, perhaps the fiercest and hottest battle of the credit crisis revolves around the issue of mark-to-market and fair value reporting standards, set by the US accounting body, FASB, and its international counterpart, which takes its cue from FASB, the IASB, Some are predicting the disappearance of jobs, many say they fear another banking crisis, depending on the outcome.

Letters pouring into the Financial Accounting Standards Board (FASB) predict those shocks and more from the rule-makers’ proposal to expand mark-to-market, or fair value accounting at US banks.

Meant to give investors more up-to-date information about banks’ financial condition, the proposal would require banks to put market values on all of their loans, even those that they don’t intend to sell. Banks now value most loans based on historical costs, a measure critics say can become outdated. The new rule would be effective in 2013, though small banks could take four more years to comply.

The proposal, partly a response to the global financial crisis, has generated fierce opposition from banks, which fear it would reduce their reported capital and require them to increase reserves. Banks argue this could discourage them from making some types of loans, hurting businesses, triggering more unemployment and harming an already fragile American economy.

Head: Robert Tweedie

Location of Head Office: London, UK

United States of America

Financial Accounting Standards Board (FASB)

Cheered by the announced retirement of FASB Chairman Robert Herz, a mark-to-market proponent, opponents have stepped up their assault. According to the American Bankers Association (ABA), a lobbying group for the $13 trillion banking industry, the change would bring about $6.7 trillion of bank loans under mark-to-market rules.

Mark-to-market critics, including members of Congress, blamed earlier tightening of fair value rules for intensifying the 2008-2009 financial crisis by triggering massive bank write-downs as prices of mortgage securities plunged. Fair value proponents dispute those claims and say more market-based information just reveals riskiness already there.

Head: Robert Herz (Outgoing)

Head Office: Norwalk, Connecticut, USA

Global

- International Organisation of Securities Commissions (IOSCO)

- Committee on Payment and Settlement Systems (CPSS)

United States of America

- The Securities & Exchange Commission (SEC)

- Commodities & Futures Trading Commission (CFTC)

European Union

- European Securities and Markets Authority (ESMA) (Formerly the Committee of European Securities Regulators (CESR)

Global

- Organisation for Economic Cooperation and Development (OECD)

Head: Angel Gurria

Head Office: Paris, France

United States of America

- Internal Revenue Service

Head: Douglas H Shulman

The head of the IRS, Commissioner of Internal Revenue, Douglas H Shulman, also chairs the OECD’s Forum on Tax Administration, which has become, under the head of the Centre of Tax Policy & Administration at the OECD, Jeffrey Owens, the main vehicle promoting Tax Information Exchange Agreements between countries, and now promises a new ‘coordination’ agenda (see also page 5) that proposes the use of joint audits between OECD member Revenue bodies and the eleven non OECD members of the FTA (Forum on Tax Administration) of the OECD.

European Union

- European Court of Justice (Supra-national appeals)

- National Revenue Services

United States of America

- North American Securities Administrators Association (NASAA)

- FINRA

The Financial Industry Regulatory Authority (FINRA) is the private-sector regulator of all securities firms doing business in the United States. It emerged in 2007 out of the consolidation of the National Association of Securities Dealers (NASD) with New York Stock Exchange Member Regulation.

European Union

- European Securities and Markets Authority (ESMA)

Global

- International Association of Insurance Supervisors (IAIS)

United States of America

National Association of Insurance Commissioners (NAIC)

European Union

- European Insurance and Occupational Pensions Authority (EIOPA) (Formerly the Committee of European Insurance and Occupational Pensions Supervisors ("CEIOPS")

Global

- Financial Action Task Force (FATF)

It is clear, however, that the new framework is just that – an empty institutional framework, that, as ever depends on the quality of the people who will drive it and staff it, and further, on the degree of sense, and consensus, that will inform the process of reforming financial centres regulation after the credit crisis. The jury remains out as to how that will pan out, because, as our review of the issues, and turf wars and controversies raging right across this international regulatory battlefield shows, the final shape of financial regulation remains to be decided.

These focus at their core on how the key issues arising from the credit crisis are being addressed. To the extent that these are being resolved, closure and progress towards stable reform will be achieved.

The credit crisis, first and foremost, was a failure of monetary policy, a view that is reflected in a paper by the chairman of the Federal Reserve Ben Bernanke in September 2010.

A major reason for this was that money supply was measured in too limited a way (and in a way that excluded the shadow banking system that grew up in the 1990s), largely beyond the attention of Central Banks.

The resolution of the banking crisis will depend on how regulators get to grips with fixing this problem, both at Central Bank level, at international cooperation level, and down to securities regulation and accounting levels. Thus issues such as central party clearing of credit derivatives arrangements are taking centre stage in the new regulatory architecture, and issues such as the Basle Committee rules for bank capital (centrally crucial), and accounting conventions, adopted by FASB and IASB, are also at the core of the story. In all of these areas, battles and controversies still rage, and how key issues are resolved will tell the tale.

At the end of the day, the credit crisis was a problem of unsound money – a problem, largely of the 2000s. Before that, the world had seen the 'death of inflation', and the decade of the 1990s ended with the price of gold at $300, down 25 p.c. on what it was a decade earlier. Now the performance of the price of gold on a daily basis is signalling to us that the problem is far from resolved. In that context, the murky shapes emerging of the new global regulatory architecture may hopefully provide optimism that a stable and solid global framework can be put in place.

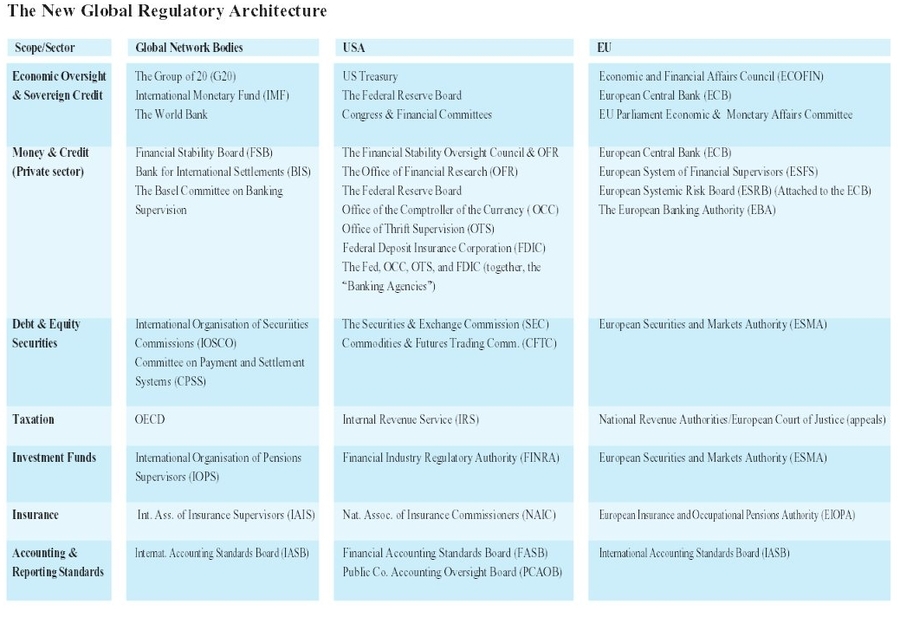

The New Global Regulatory Architecture

Economic Oversight & Sovereign Credit

Global

The Group of 20 (G20)

The Group of 20 morphed out (in 2008) of the G7 and G8 of the 1970s and 1980s as the bi-annual forum of global heads, at times meeting to coordinate macro-economic strategies to becoming the primary politicians forum for agreeing joint initiatives about the regulatory and banking framework. As a political forum its antecedents stretch back in history, some might argue going back, perhaps, to the Treaty of Vienna, or even before, the Treaty of Westphalia (1648).

Today it drives the tax agenda of the OECD, and bank regulatory matters. Its expansion from the G8 to the G20 was also accompanied by a more specific financial stability mandate. Its next meeting is in Seoul in November. However, as with all global bodies, its powers are suasive, and informal, and derive their force from reputational force, such as the OECD 'name and shame' approach of publishing blacklists of aberrant 'tax havens'.

Head: Lee Myung-bak

Head Office (Current): Seoul, Rep Korea

International Monetary Fund (IMF)

The IMF, like its counterparts, the World Bank, and the OECD, are institutions that were formed at Bretton Woods, at the seminal gathering of victorious governments after WW2, and which approved the 'Marshall Plan' for the aiding of recovery in Europe. These bodies were set up as part of the Marshall Plan architecture.

The IMF today has a newly rejuvenated role, thanks to sovereign debt difficulties, most notably in Europe, and its role in coordinating finance from member states in general, as well as the European Union to aid Greece, represented an internationalisation of the debt crisis beyond the confines of the European Union. It may also gain enhanced influence in the currency policy sphere.

Head: Dominique Strauss-Kahn

Head Office: Washington, DC, USA

The World Bank

The World Bank, with its developmental mandate continues to pursue supplementary support programs, as well as support activities such as the publication of its influential 'Ease of Doing Business' Surveys.

Head: Robert Zoellick

Head Office: Washington, DC, USA

United States of America

US Treasury

In pole position, the US Treasury will orchestrate the workings of the newly established Financial Stability Oversight Council, through its secretariat, The Office of Financial Research (OFR), which will operate from within the Treasury Department.

Head: Timothy Geithner

Head Office: Washington, DC, USA

The Federal Reserve Board

The Dodd Frank Bill has unleashed the so-called “Banking Agencies” with new powers that raises their status to that of the Fed on the Financial Stability Oversight Council. The fears are that these will prove a route for political interference with Fed oversight and enforcement of monetary policy.

Head: Ben Bernanke

Head Office: Washington, DC, USA

Congress & Financial Committees

Congressional representatives, and committees, for example the Financial Crisis Committee, which reports this Fall, exert major influence, which can find their way into interference in policy via the new channels opened up by Dodd-Frank.

Head: Nancy Pelosi

Head Office: Washington, DC, USA

European Union

Economic and Financial Affairs Council (ECOFIN)

Chair: Didier Reynders, Belgian Deputy PM and Minister for Finance

The Council of Finance Ministers of the sovereign members of the European Union. The European Parliament proposes, and votes on EU supranational legislation, drafted by the European Commission, which is the civil service of the EU, directed by EU Commissioners, each appointed for a term co terminus with the life of the European Parliament. Financial services regulation is the responsibility of DG Markt (Internal Market Directorate) (Head: Commissioner Michel Barnier), and credit and banking DG ECFIN (Commissioner Olli Rehn). The EU Parliament Economic & Monetary Affairs Committee appointed from MEPs (Chair: Sharon Bowles MEP) oversees legislation and financial services regulatory affairs.

European Central Bank (ECB)

The ECB, as the federal central bank for the euro, is in the eye of the global financial storm, alongside its US counterpart, the Fed. As architect of the first major truly global currency in history, the experiment of the euro has been tarnished by the credit crisis, and, latterly by the sovereign debt crisis in the EU. The president of the ECB JC Trichet has been reaffirmed as pole player in charge of the new EU Bank regulatory body, the European Systemic Risk Board (ESRB) attached to the ECB.

CEO: Jean Claude Trichet

Head Office: Frankfurt, Germany

Money & Credit (Private sector)

Global

Financial Stability Board (FSB)

The FSB, a good idea in theory, but possibly bad in practice, is lauded as the ‘potential fourth pillar of the Bretton Woods system’ is perhaps the most obvious early creation of the credit crisis. It sprung from the idea that because the credit crisis was 'global' what was needed was a global body that dealt with global systemic risk issues. The danger, as with all such bodies, is that it might distract attention from the role of national central banks in running their own money supplies, and regulating their own banking, and shadow banking systems. The most important potential role for the FSB would be the promotion of currency stability (and flexibility) in the world, so that countries and currency zones pursuing sound money strategies (a) could be persuaded of the value of sound money, and strong currencies, and (b) encouraged, or incentivised in some way, to pursue such strategies. As Asia, and Asian centres have been exemplary in the 2000s, compared with their Atlantic counterparts, perhaps the headquarters of the FSB could be moved to Beijing at an appropriate time in the future, with the Chinese dropping as a quid pro quo their suggestion that IMF SDRs replace the US dollar as the de facto global reserve currency?

HEAD: Mario Dhragi

Head Office: Basle, Switzerland

The Basel Committee on Banking Supervision/Bank for International Settlements (BIS)

When the history of the 21st century's credit crisis (history's first credit derivatives crisis) is written, the potential role of the Basle Committee in defining the new global ground rules for bank leverage, may loom large. If it does so wisely, including sensible measures for the measurement of bank capital, and how credit derivatives should be properly accounted for in the future, it will emerge as having a pivotal role.

Head: Nout Wellink

Head Office: Basle, Switzerland

United States of America

- The Financial Stability Oversight Council & OFR

- The Office of Financial Research (OFR)

- The Federal Reserve Board

- Office of the Comptroller of the Currency ( OCC)

- Office of Thrift Supervision (OTS)

- Federal Deposit Insurance Corporation (FDIC)

- The Fed, OCC, OTS, and FDIC (together, the “Banking Agencies”)

European Union

- European Central Bank (ECB)

- European Systemic Risk Board (ESRB) (Attached to the ECB)

- European System of Financial Supervisors (ESFS)

- The European Banking Authority (EBA)

Accounting & Reporting Standards

Global

International Accounting Standards Board (IASB)

Indicating that true global leadership in finance remains in the United States, perhaps the fiercest and hottest battle of the credit crisis revolves around the issue of mark-to-market and fair value reporting standards, set by the US accounting body, FASB, and its international counterpart, which takes its cue from FASB, the IASB, Some are predicting the disappearance of jobs, many say they fear another banking crisis, depending on the outcome.

Letters pouring into the Financial Accounting Standards Board (FASB) predict those shocks and more from the rule-makers’ proposal to expand mark-to-market, or fair value accounting at US banks.

Meant to give investors more up-to-date information about banks’ financial condition, the proposal would require banks to put market values on all of their loans, even those that they don’t intend to sell. Banks now value most loans based on historical costs, a measure critics say can become outdated. The new rule would be effective in 2013, though small banks could take four more years to comply.

The proposal, partly a response to the global financial crisis, has generated fierce opposition from banks, which fear it would reduce their reported capital and require them to increase reserves. Banks argue this could discourage them from making some types of loans, hurting businesses, triggering more unemployment and harming an already fragile American economy.

Head: Robert Tweedie

Location of Head Office: London, UK

United States of America

Financial Accounting Standards Board (FASB)

Cheered by the announced retirement of FASB Chairman Robert Herz, a mark-to-market proponent, opponents have stepped up their assault. According to the American Bankers Association (ABA), a lobbying group for the $13 trillion banking industry, the change would bring about $6.7 trillion of bank loans under mark-to-market rules.

Mark-to-market critics, including members of Congress, blamed earlier tightening of fair value rules for intensifying the 2008-2009 financial crisis by triggering massive bank write-downs as prices of mortgage securities plunged. Fair value proponents dispute those claims and say more market-based information just reveals riskiness already there.

Head: Robert Herz (Outgoing)

Head Office: Norwalk, Connecticut, USA

Debt & Equity securities

Global

- International Organisation of Securities Commissions (IOSCO)

- Committee on Payment and Settlement Systems (CPSS)

United States of America

- The Securities & Exchange Commission (SEC)

- Commodities & Futures Trading Commission (CFTC)

European Union

- European Securities and Markets Authority (ESMA) (Formerly the Committee of European Securities Regulators (CESR)

Taxation

Global

- Organisation for Economic Cooperation and Development (OECD)

Head: Angel Gurria

Head Office: Paris, France

United States of America

- Internal Revenue Service

Head: Douglas H Shulman

The head of the IRS, Commissioner of Internal Revenue, Douglas H Shulman, also chairs the OECD’s Forum on Tax Administration, which has become, under the head of the Centre of Tax Policy & Administration at the OECD, Jeffrey Owens, the main vehicle promoting Tax Information Exchange Agreements between countries, and now promises a new ‘coordination’ agenda (see also page 5) that proposes the use of joint audits between OECD member Revenue bodies and the eleven non OECD members of the FTA (Forum on Tax Administration) of the OECD.

European Union

- European Court of Justice (Supra-national appeals)

- National Revenue Services

Investment Funds

United States of America

- North American Securities Administrators Association (NASAA)

- FINRA

The Financial Industry Regulatory Authority (FINRA) is the private-sector regulator of all securities firms doing business in the United States. It emerged in 2007 out of the consolidation of the National Association of Securities Dealers (NASD) with New York Stock Exchange Member Regulation.

European Union

- European Securities and Markets Authority (ESMA)

Insurance

Global

- International Association of Insurance Supervisors (IAIS)

United States of America

National Association of Insurance Commissioners (NAIC)

European Union

- European Insurance and Occupational Pensions Authority (EIOPA) (Formerly the Committee of European Insurance and Occupational Pensions Supervisors ("CEIOPS")

Crime Enforcement

Global

- Financial Action Task Force (FATF)

|